What is Accounting?

Accounting is the process of identifying, measuring, recording and communicating the required information relating to the economic events of an organisation to the interested users of such information.

Table of Content

Definition of Accounting

Accounting as the art of recording, classifying, and summarising in asignificant manner and in terms of money, transactions and events which are, in part at least, of financial character, and interpreting the results thereof. – The American Institute of Certified Public Accountants (AICPA)

Accounting as ‘the process of identifying, measuring and communicating economic information to permit informed judgments and decisions by users of information’. – American Accounting Association (AAA)

The Accounting Principles Board of AICPA also emphasised that the function of accounting is to provide quantitative information, primarily financial in nature, about economic entities, that is intended to be useful in making economic decisions.

Objectives of Accounting

Following are objectives of accounting which given below:

- Maintenance of Records of Business Transactions

- Calculation of Profit and Loss

- Depiction Of Financial Position

- Providing Accounting Information To Its Users

Maintenance of Records of Business Transactions

Accounting is used for the maintenance of a systematic record of all financial transactions in book of accounts. Even the most brilliant executive or manager cannot accurately remember the numerous amount of varied transactions such as purchases, sales, receipts, payments, etc. that takes place in business everyday.

Calculation of Profit and Loss

‘Profit/loss’ is a core accounting measurement. It is measured by preparing profit and loss account for a particular period. Various other accounting measurements such as different types of revenue expenses and revenue incomes are considered for preparing this profit and loss account.

The owners of business are keen to have an idea about the net results of their business operations periodically, i.e. whether the business has earned profits or incurred losses. Difference between these revenue incomes and revenue expenses is known as result of business transactions identified as profit/loss.

Depiction Of Financial Position

Accounting also aims at ascertaining the financial position of the business concern in the form of its assets and liabilities at the end of every accounting period. A proper record of resources owned by business organisation (Assets) and claims against such resources (Liabilities) facilitates the preparation of a statement known as balance sheet position statement.

Financial position’ is another core accounting measurement. Financial position is identified by preparing a statement of ownership i.e., Assets and Owings i.e., liabilities of the business as on a certain date.

Providing Accounting Information To Its Users

The accounting information generated by the accounting process is communicated in the form of reports, statements, graphs and charts to the users who need it in different decision situations.

The primary objective of accounting is to provide useful information for decision-making to stakeholders such as owners, management, creditors, investors, etc. Various outcomes of business activities such as costs, prices, sales volume, value under ownership, return of investment, etc. are measured in the accounting process.

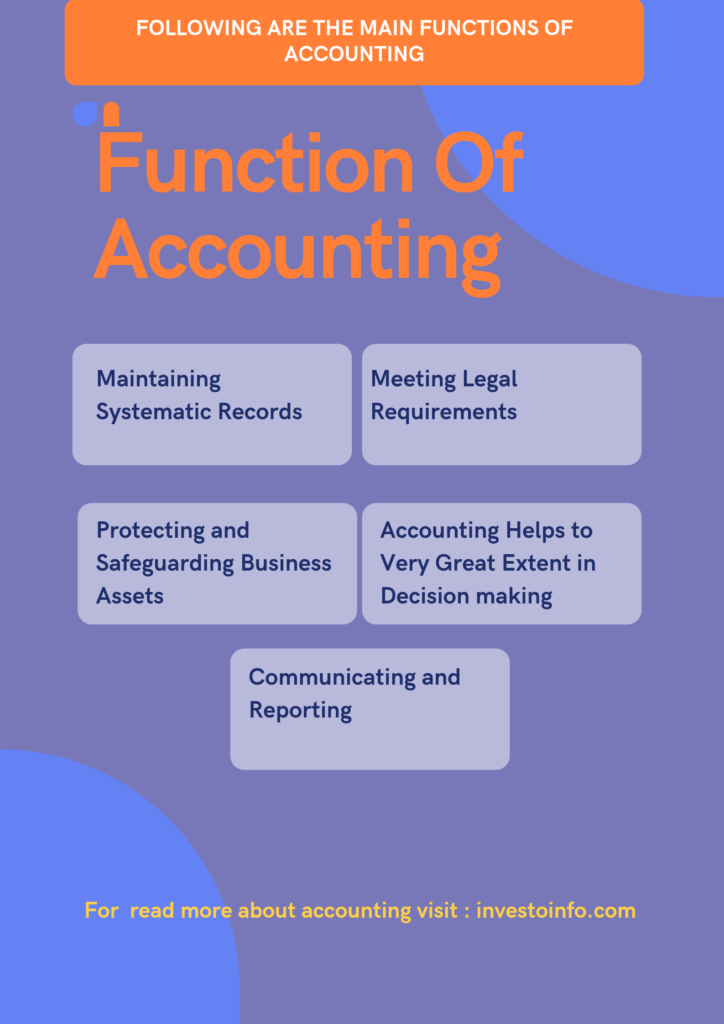

Function Of Accounting

Following are the main functions of accounting:

- Maintaining Systematic Records

- Meeting Legal Requirements

- Protecting and Safeguarding Business Assets

- Accounting Helps to Very Great Extent in Decision making

- Communicating and Reporting

Maintaining Systematic Records

The basic function of accounting is to maintain proper records of transactions that take place in chronological order. These records provide a base analysis and decision-making. It consists of recording in the original/subsidiary books of entry, posting to ledger, preparation of trial balance and final accounts.

Meeting Legal Requirements

Under the provision of law, a business person has to file various statements e.g. income tax returns, returns for sales tax purpose etc. Accounting system aims at fulfilling the requirements of law. Accounting is a base, with the help of which various returns, documents, statements etc are prepared.

Protecting and Safeguarding Business Assets

Records always serve as an evidence in case of any dispute relating to ownership title of any property or assets of the business. Accounting helps in this regard to a very great extent it protects the property of business from unjustified and unwanted use. The accounts manager thus has to design such a system of accounting, which protects its assets from an unjustified and unwanted use.

Accounting Helps to Very Great Extent in Decision making

The accounting facilitates the right decision-making process. Most of the managerial decisions are based on the figures. An effective price policy, satisfied wage structure, inventory policy, advertisement and sales promotion policy are a result of proper accounting structure. Accounting provides necessary data on which managerial decision-making process is based.

Communicating and Reporting

Accounting can be said to be the language of business. All the transactions of business are communicated through accounting. All the interested parties such as entrepreneur, creditors, governments, and employees and so on, who are interested directly or indirectly in knowing the results of the firm are provided information through accounting.

Need for Accounting

Need for accounting are :

Accounting is often called the speech of business. It serves as means of communication. The information regarding the results of business operations to interested parties in the business viz., the proprietor, creditors, government and other agencies are to be communicated in the form of accounting data.

In order to provide correct information it is necessary for the business organisation to record its transactions in clear and systematic manner. A clear and systematic record will serve twin purposes like

- Ascertaining transactions of business to determine profits or loss made during any accounting period.

- Showcase of impact of business transactions on the net worth of the business unit i.e. financial position of the business in terms of assets and liabilities of business as a whole.

Since resources are scarce, it is wiser to maintain a check on them constantly, to know whether there has been any generation of income or squeezing or shrinking of resources. It is of primary importance and is considered an indispensable tool of measuring operating efficiency of any profit making or non- profit making entity.

Users of Accounting Information

Accounting information is of prime importance to its interested parties to understand the financial position of firm and its future prospects. The interested parties or users of accounting can be divided into two main categories namely, external and internal users.

External User of accounting information

Creditors

People who have extended credit to the company are termed as creditors. They are eager to know the financial position of firm to determine whether the enterprise will be able to meet its obligations in time. The statement of accounts helps to determine a liquidity position on which creditors can rely upon and check their credit policy or supply decisions.

Investors

These individuals put their money in any business with the aim of making more money. Any investor before making investments considers three important factors i.e. safety of his principle amount, rate of return on his investment in the form of dividend/interest and regular and consistent rate of return. Detailed study of the financial statements of firm enables investors in taking correct investment decision.

Government

The government is not interested in making money or investments. It is concerned with accounting information of company for purpose of taxation, labour and corporate law. Thus, it is interested in allocation of resources, taxation policies and statistical interests.

Bankers

Banks and financial institutions who lend money to business want to know the financial stability of the company in terms of the company ability to pay interest and principle amount. They want to know whether this company can turn into a defaulter if so banks would not want to lend to such company.

Competitors

Competitors of the company are interested in its financial to improve its own financial strategies, policies and systems.Comparison of one company with another can provide valuable clues about the financial health of the organisation. It helps to benchmark its own financial results.

Others

In addition to the above, other users of accounting information are researchers, consumers, stock exchange, brokers, underwriters, economists, press and public in general. However, their interests and goals altogether being different in nature, yet require accounting information for serving their own interests.

Internal Users of Accounting Information

Owners

Owners include shareholders, partners and proprietors of the firm. They are the backbone of the business in the sense that they provide necessary funds for its smooth running, growth and development. Company’s profitability and financial security are, therefore of prime importance to these people who have stake in the business. Such information can be obtained through published accounts, annual report and other supplementary statements.

Management

Accounting provides necessary information for managerial decision-making. The managerial tools, such as production budget, sales budget and cash budget, capital budget, etc., are the result of efficient accounting system. Various functions of management such as planning, organising, coordination, motivation and control can be implemented effectively through proper accounting system.

Employees

Healthy industrial relations between employer and employee are important to growth and development of firm. Accounting information helps to settle industrial disputes, prevent strike or likewise situation arising from demand for wage hike, bonus, higher compensation, etc. It helps employees to determine whether they are paid fair wages or not.

Types of Accounts

An account can be explained as a summary record of all transactions related to a particular type of item. It may be an asset, a liability, income, expenses, etc. These accounts are then classified in different types. There are two types of accounts are :

Personal Account

Personal accounts include the accounts of persons with whom the business deals. These accounts show the transactions with the clients, suppliers, money lenders, bank, etc. The main purpose of preparing personal accounts is to ascertain the balances due to or due from persons or organisation.

Impersonal Accounts

The accounts other than personal accounts are termed as impersonal accounts and divided into two parts, real and nominal.

Real Accounts

Accounts of each property or assets acquired by the firm named real accounts. These accounts are both tangible and intangible. Tangible real accounts relate to the real properties, which we can see, touch, or feel, such as building furniture, etc. Intangible real accounts consists of such things, which cannot be touched but may be measured in terms of money, such as Goodwill, trademarks, patents, etc.

Nominal Accounts

These are the accounts of incomes, expenses, gains and losses. The business has to incur certain expenses to earn certain income or to meet the requirements or certain business transaction. As for illustration these accounts are rent, wages or salary paid, telephone expenses, purchase, sale, etc.

Table Types of Accounts

| Type | Represent | As for illustrations |

| Real | Tangible things which are available physically in the real world and certain intangible things not existing physically | Tangibles – Plant and Machinery, Furniture and Fixtures, Computers and Information Processing Equipment etc., Intangibles – Goodwill, Patents and Copyrights |

| Personal | Legal and Business Entities (Natural and artificial persons) | Individuals, Partnership Firms, Corporate entities, Non-Profit organisations, any local or statutory bodies including local, state and national governments |

| Nominal | To recognise the implications of financial transactions during each fiscal year till finalisation of accounts at the end, Income and Expenditure Accounts are Temporary accounts. | Sales, Purchases, Electricity Charges, Commission, Rent, Interest. |

Rules of Debit (Dr.) and Credit (Cr.)

There are rules for every type of account whether it is credit or debit. Let us study those rules in detail now.

| Personal Account | Real Account | Nominal Account |

| Debit the Receiver And Credit the Giver | Debit whatever come in Credit whatever goes out | Debit all expenses & losses credit the incomes & gains. |

FAQ

What is Accounting?

Accounting is the process of identifying, measuring, recording and communicating the required information relating to the economic events of an organisation to the interested users of such information